$NBIS - Nebius: The Compute Landlord

An eighteen-month-old "startup”, today sits in the Nasdaq-100 with multi-year contracted demand giving revenue visibility into the early 2030s, and it cannot build fast enough to fill it.

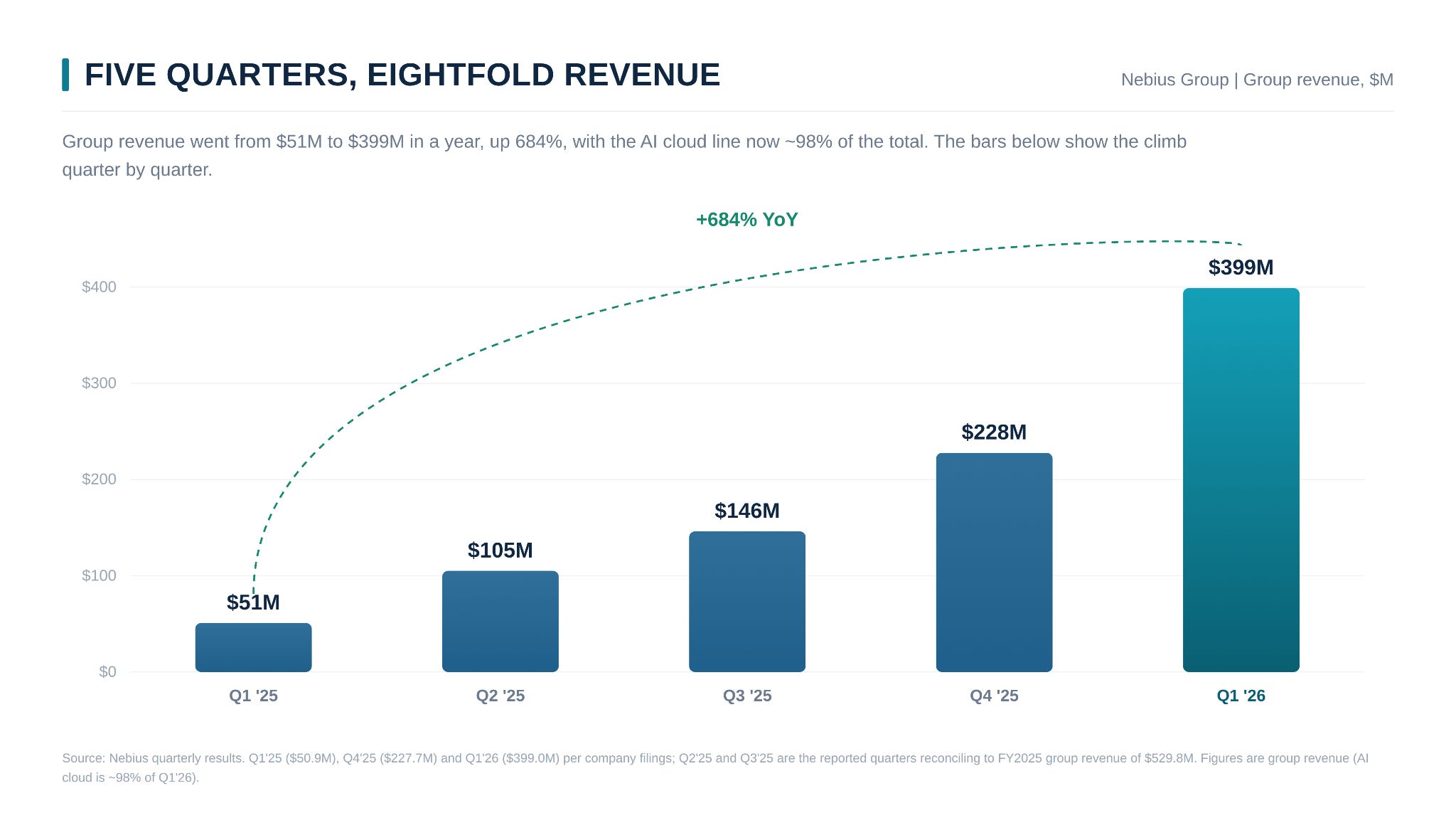

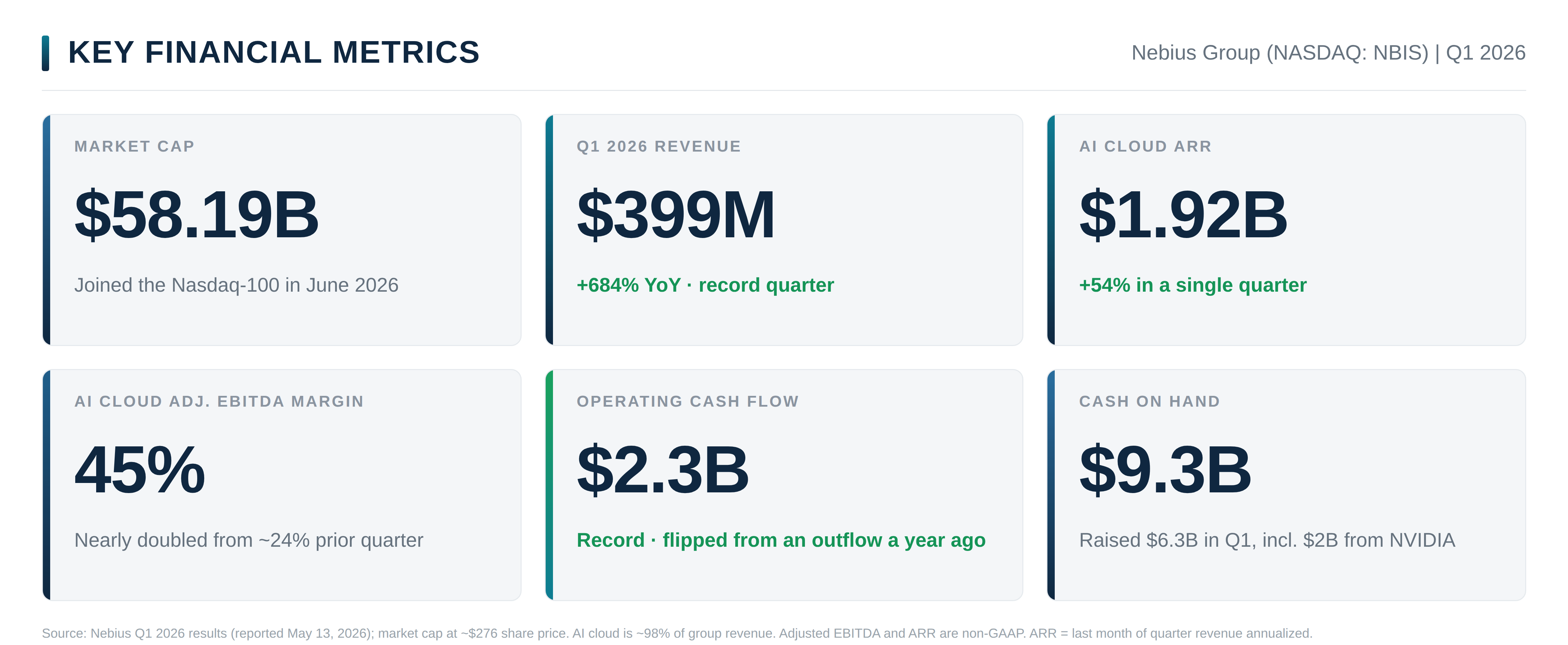

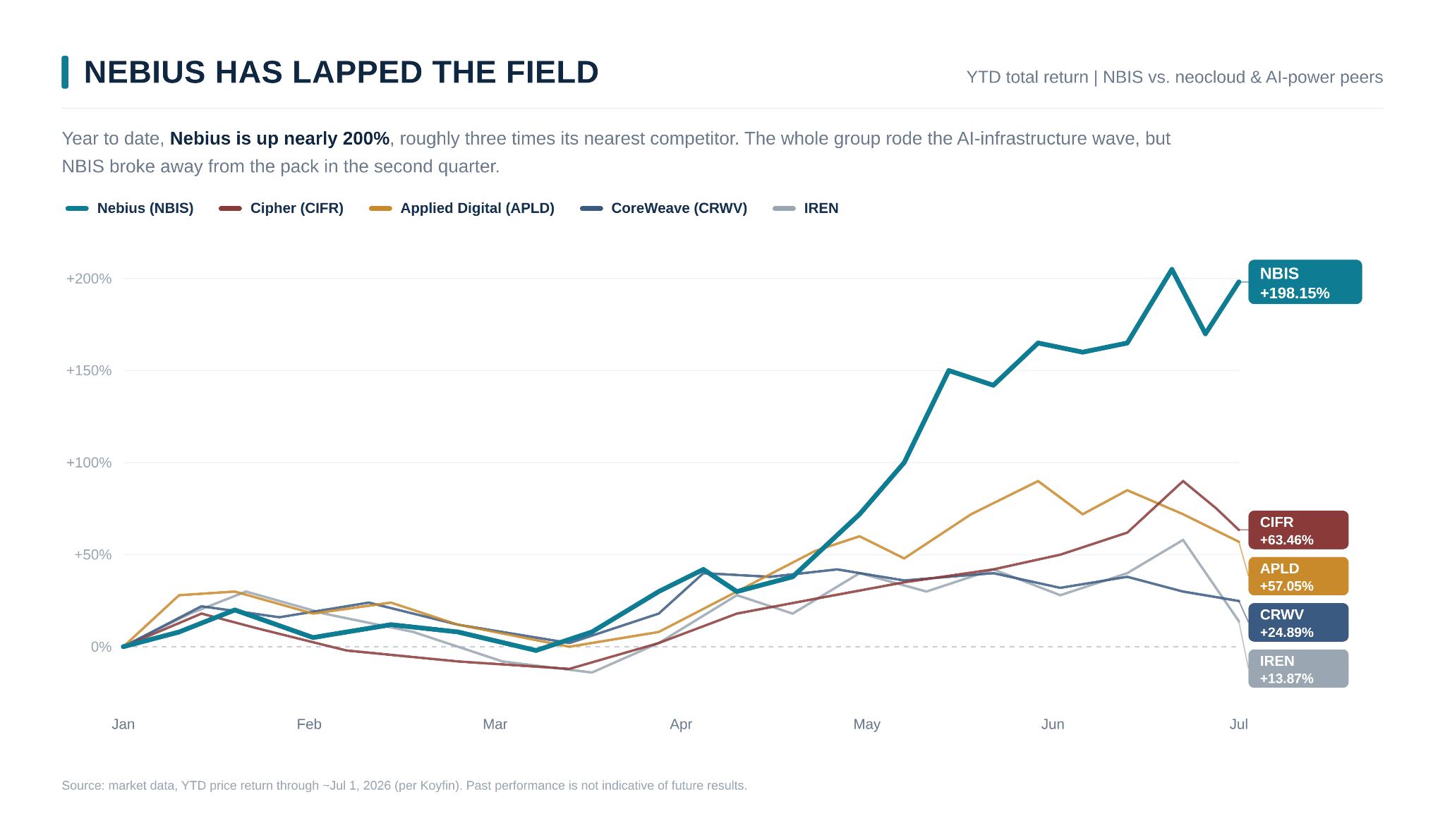

From $44 a year ago to roughly $230 today, up more than 450% in twelve months. The Q1 print in May was not subtle: revenue of $399 million, up 684% year over year, with core AI cloud ARR exiting the quarter at $1.92 billion. The market cap now sits near $60 billion. Market figures here are a snapshot as of early July 2026 and move fast.

BEFORE WE DIVE IN

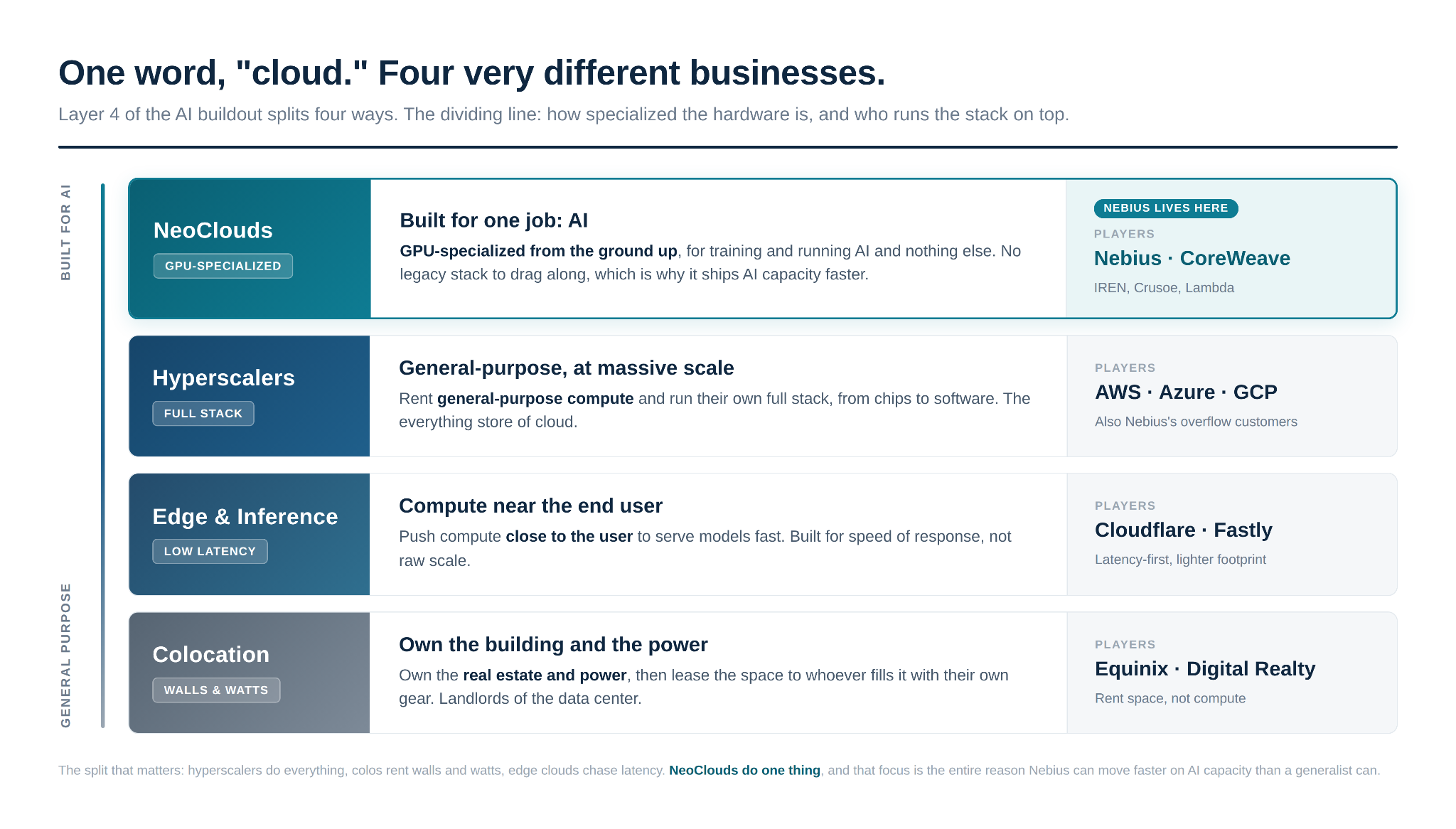

Nebius sits at Layer 4: Cloud Infrastructure. This is the layer that takes all the silicon underneath, the GPUs, the memory, the interconnect, and assembles it into something a customer can actually use: powered, cooled, networked, and rented out by the hour.

Layer 4 has four buckets:

Hyperscaler clouds (AWS, Azure, GCP) rent general-purpose compute at massive scale and run their own full stack.

Data center colocation providers own the buildings and the power, then lease that space to whoever fills it.

Edge and inference clouds push compute close to the end user to serve models with low latency.

NeoClouds, the bucket Nebius lives in, are GPU-specialized from the ground up: built for one job, training and running AI, and nothing else.

Nobody trains a frontier model on a chip. They train it on a cluster: thousands of GPUs wired together, fed by memory and interconnect, sitting inside a building that draws the power of a small city. Building that building, filling it, and keeping it running at high utilization is its own bottleneck, and it is the one the NeoClouds solve.

The shortest version of the thesis: the hyperscalers committed to spend hundreds of billions on AI through 2027, and they physically cannot pour concrete and rack GPUs fast enough to keep up with their own demand. So they are outsourcing the overflow. Microsoft and Meta, two companies that build data centers for a living, looked at their own buildout timelines and decided it was faster to rent capacity from Nebius than to wait on their own. That is the name of the game. The compute crunch is so severe that the buyers who build are now renting.

Nebius is one of a small handful of independent “neoclouds” positioned to catch that overflow. Nebius is the one that owns its full stack, from the data center design down to the servers and racks, and it is the one that walked into this market with a Nasdaq listing already in hand.

Before we go further, a note on what makes this name different from the rest of the AI trade. Most of the supply chain is a parts business: you sell a chip, a substrate, a laser, a stack of memory. Nebius sells time on a machine it owns. That changes the economics, the risks, and the valuation math completely, and it is the whole reason the stock looks the way it does.

SECTION 1 · COMPANY SNAPSHOT

What is NBIS and how did a Yandex spinoff end up in the Nasdaq-100?

First, what it is today. Nebius calls itself "the AI cloud company": a single platform that covers the whole AI journey, from data and model training to tuning, inference, and deployment, built on deep in-house engineering and already serving enterprises across healthcare, robotics and physical AI, financial services, media, and retail. It is headquartered in Amsterdam and trades on Nasdaq as $NBIS. That positioning matters because AI is shifting from research into large-scale production, and production is where cloud infrastructure gets reshaped.

Now the strange part: where it came from. Nebius is what was left of Yandex, the “Google of Russia,” after the 2022 war forced a split. Yandex sold its entire Russian business and kept the assets that sat outside Russia: a data center in Finland, a self-driving unit, a data-labeling business, an edtech platform, and roughly $2.5 billion in cash. Founder Arkady Volozh renamed those pieces Nebius Group and resumed trading on Nasdaq in October 2024.

So this is a “startup” that is already public, with real operating history and a founder who has built a continental-scale tech company once before. Volozh took Yandex to a $30 billion peak. He is now doing it a second time, in a new country, in the most capital-intensive corner of the hottest market in tech.

For most of 2025 the stock flew under the radar. Then the contracts landed: $17.4 billion from Microsoft, a Meta deal that grew from $3 billion to $27 billion, and a $2 billion equity check from NVIDIA. The market repriced the company in months. Shares ran from the low $40s to a high near $300, Nebius joined the Nasdaq-100 in June 2026, and a hedge fund run by former OpenAI researcher Leopold Aschenbrenner disclosed a 5.6% stake worth about $2.6 billion, its single largest position. The leftover asset became one of the most fought-over names in AI infrastructure.

SECTION 2 · FUNDAMENTALS

How does it make money and who’s running the show?

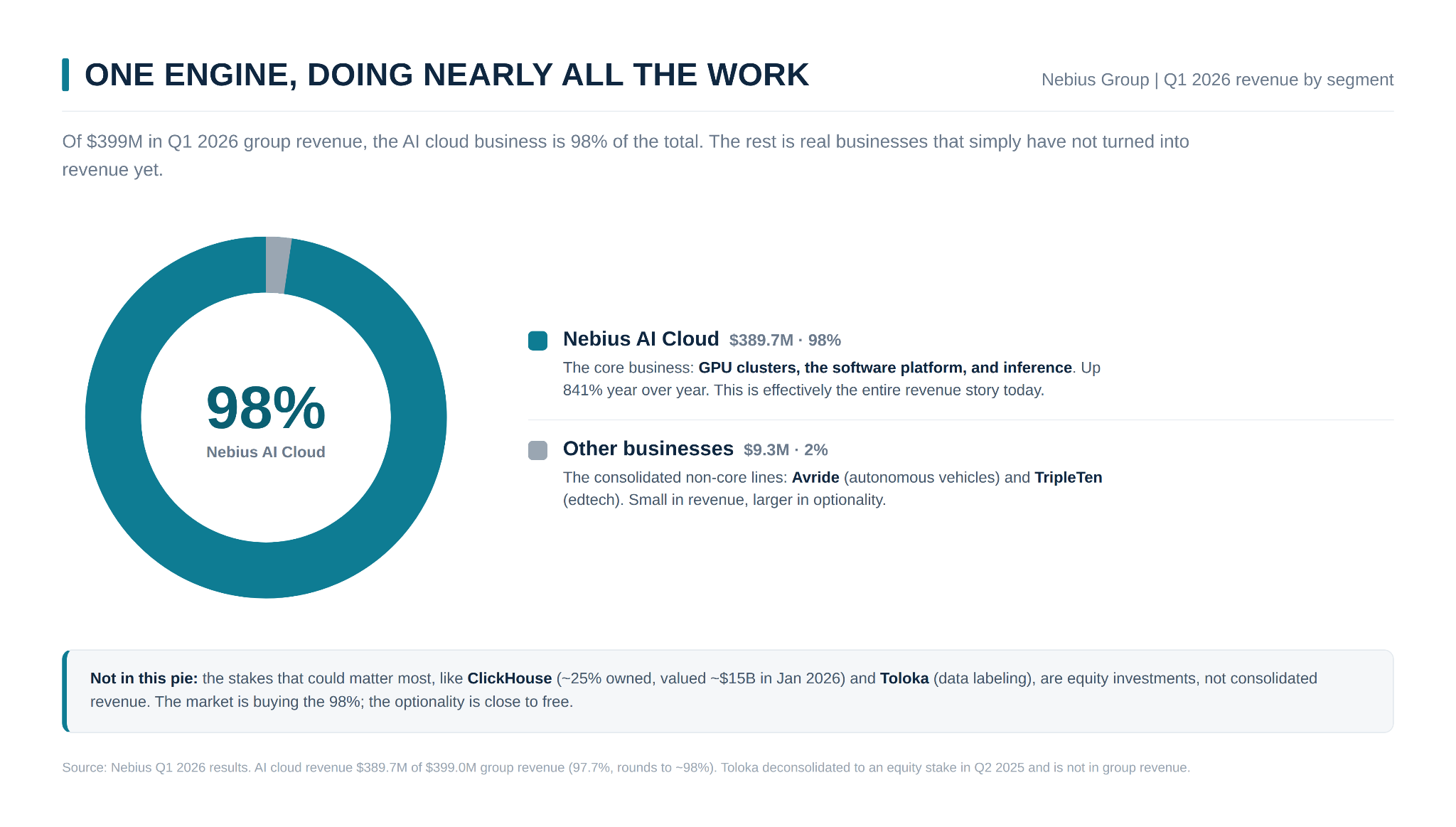

Nebius organizes around one core business and a cluster of optionality. The core is Nebius AI Cloud: large-scale GPU clusters, a full software platform on top, and developer tools for training and running models. In Q1 2026 it did $389.7 million of revenue, about 98% of the group. Everything else is upside that has not been priced yet.

The model is straightforward to describe and brutal to execute. Nebius secures power and land, builds or leases data centers, fills them with NVIDIA GPUs, wraps its own software stack around the hardware, and sells access. The differentiator it leans on is vertical integration: it designs its own servers, racks, and connectivity rather than just renting bare metal, which it argues lets it ship capacity faster and run it at higher margins. Volozh frames the constraint the same way every quarter: this is a supply problem, not a demand problem. On the Q1 call, management said demand was vastly exceeding capacity and that pipeline generation hit a record, up roughly 3.5x quarter over quarter.

The management team

Three seats matter most, and each maps to something Nebius specifically needs.

Founder and CEO Arkady Volozh built Yandex into a $30 billion company over two decades. Having built a continental-scale tech company once already, he is the rare operator with the conviction and the credibility to bet tens of billions on a GPU buildout and make hyperscalers believe he can deliver it.

CFO Dado Alonso joined in 2025 from Amazon, Booking.com, and Naspers/OLX. At Nebius the funding model is the business model: someone has to structure asset-backed financing against multi-year hyperscaler contracts while managing dilution on a company raising billions a quarter. That makes the finance seat the most important operational seat in the building, and it is held by someone from high-growth tech finance, not a sleepy treasury desk.

CRO Marc Boroditsky joined in 2025 after growing Twilio’s revenue more than 10x to $4 billion. You do not hire a closer of that caliber unless you plan to keep signing contracts the size of the Microsoft and Meta deals already on the books.

Who actually buys from Nebius?

Two names dominate, and that is both the bull case and the bear case in one breath.

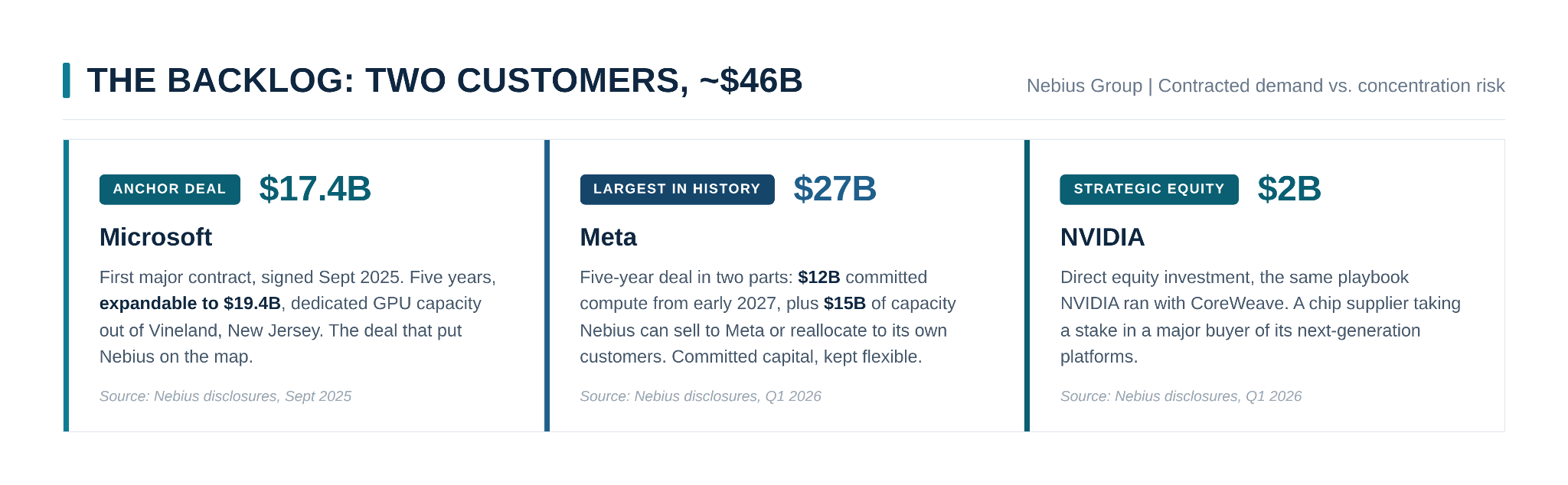

Microsoft was first. In September 2025, Nebius signed a five-year deal worth $17.4 billion, expandable to $19.4 billion, supplying dedicated GPU capacity out of a new data center in Vineland, New Jersey. It was Nebius’s first contract with a major tech player, and Volozh said at the time he expected “more to come.” He was right.

Meta came next, and the structure is worth reading closely because it is more than a headline number. The latest agreement is a $27 billion, five-year deal, the largest in Nebius’s history, and it comes in two parts: a $12 billion, five-year purchase of dedicated compute capacity scheduled to begin in early 2027, plus up to $15 billion more that Nebius can sell to Meta on pre-agreed terms, or to its own AI cloud customers at market rates. That second leg is the clever bit. It is committed capital and long-term visibility, but Nebius keeps the option to reallocate the capacity if it finds a better home for it. The same month, NVIDIA invested $2 billion directly into Nebius, the same playbook it ran with CoreWeave, securing a strategic foothold in a buyer of its next-generation platforms.

Stack those together and Nebius entered the back half of 2026 with a backlog around $46 billion, the overwhelming majority of it Microsoft and Meta.

Sit with that. A roughly $3 billion revenue company is sitting on a $46 billion order book, and two customers are most of it. That is demand visibility most infrastructure businesses would kill for. It is also a dependency most would lose sleep over. Both are true at once. That is what owning Nebius means right now.

SECTION 3 · FINANCIAL PROFILE

Nebius has crossed from obscure spinoff into one of the fastest-growing names in public markets, and Q1 2026 is where the growth became impossible to argue with.

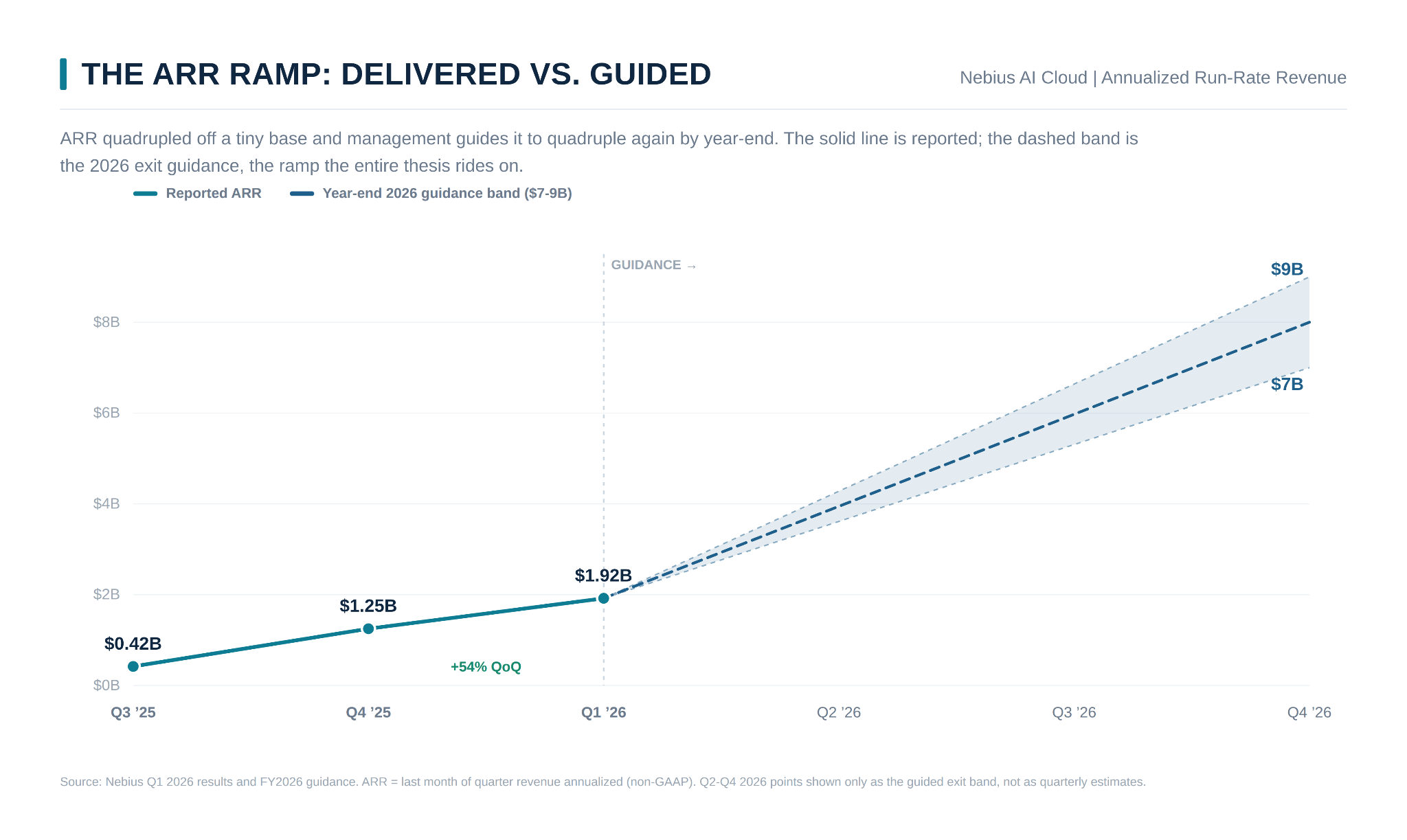

Revenue hit $399 million, up 684% in a year. The core AI cloud business did better still, up 841% to $390 million, now 98% of the company. The number the Street actually tracks is ARR (annual run-rate, basically the last month’s revenue times twelve), and it jumped 54% in a single quarter to $1.92 billion. For scale: Nebius did $530 million in all of 2025. It just exited a quarter running at nearly four times that.

The profitability turn is real, but read it carefully. On an adjusted-EBITDA basis (rough operating profit), the AI cloud unit cleared a 45% margin, almost double the prior quarter, and management is steering toward 20-30% operating margins. The headline GAAP profit of $621 million, though, is mostly a $781 million paper gain on its ClickHouse stake, not money earned. Strip that out and the business still runs a loss, and the cleaner figure actually got worse: an adjusted net loss of $100 million versus $84 million a year ago. Scaling toward profit, not there yet.

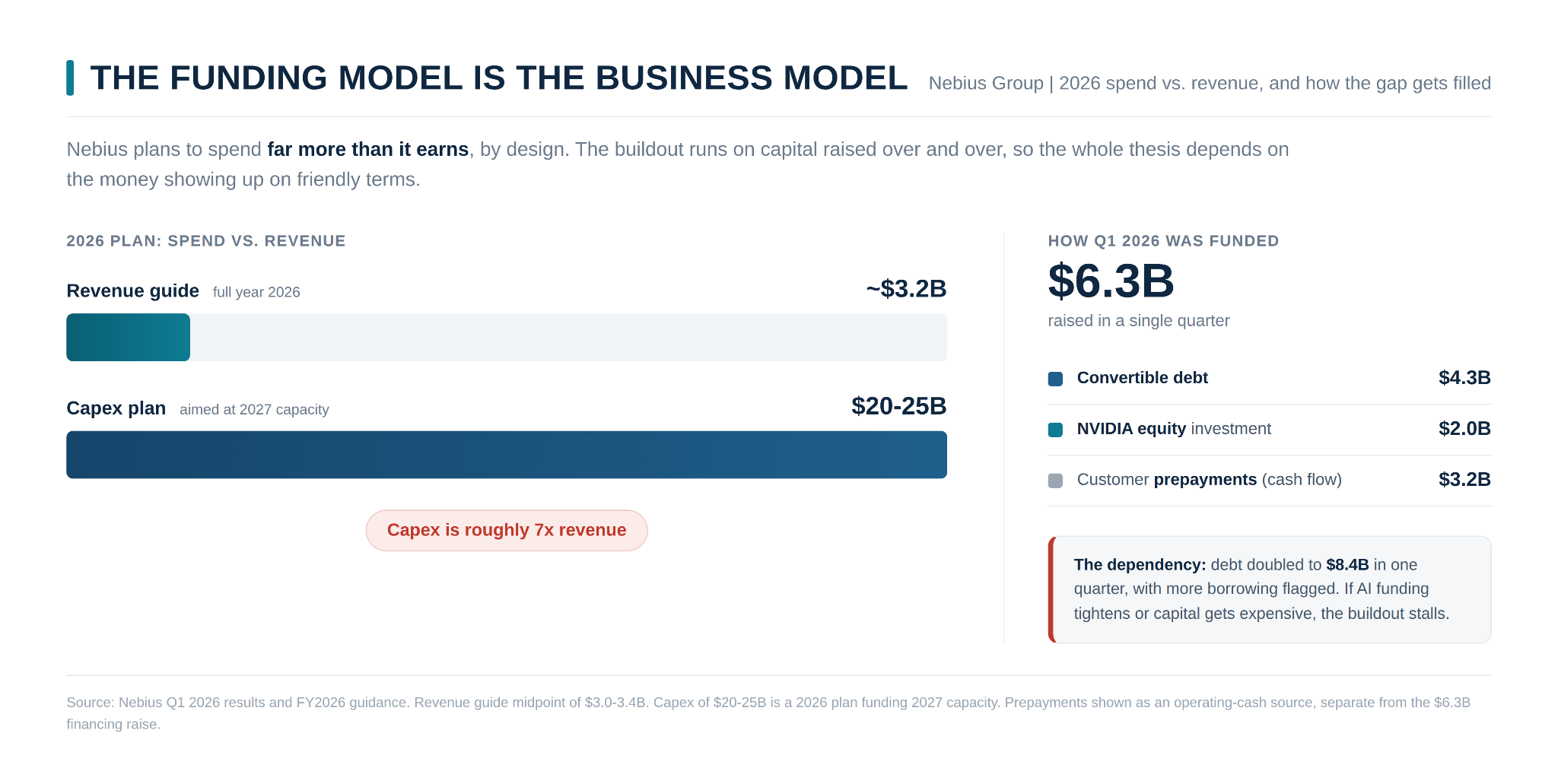

Cash flow is the interesting part. Operating cash flow hit a record $2.3 billion, swinging from an outflow a year earlier, almost entirely because customers pay upfront. Those prepayments dropped $3.2 billion into the quarter and sit at $4.8 billion on the balance sheet. Cash on hand is $9.3 billion. But the appetite is enormous: Nebius raised $6.3 billion in Q1 alone ($4.3 billion in convertible debt plus NVIDIA’s $2 billion equity check), and debt doubled to $8.4 billion in three months. That is the tell. This business burns capital as fast as it grows, and the whole thesis rides on it raising more on friendly terms.

For 2026, management guides to $3.0-3.4 billion in revenue, $7-9 billion ARR by year-end, and roughly 40% margins, funded by a staggering $20-25 billion capex budget aimed at 2027 capacity.

The number that matters most is power. Contracted capacity is now 3.5 GW and climbing past a raised 4 GW target, with Nebius owning over 75% of it. Live, revenue-generating capacity should hit 800-1,000 MW by year-end, up from just 170 MW. That is a five-to-six-fold expansion in twelve months, and the footprint went from one large site to seven.

Bottom line: few companies in public markets are compounding this fast, the core engine is turning profitable, and the balance sheet is being levered hard to build capacity that is mostly pre-sold. The question was never whether Nebius is growing. It is whether the money keeps showing up without crushing the stock.

SECTION 4 · PRODUCT AND TECHNOLOGY

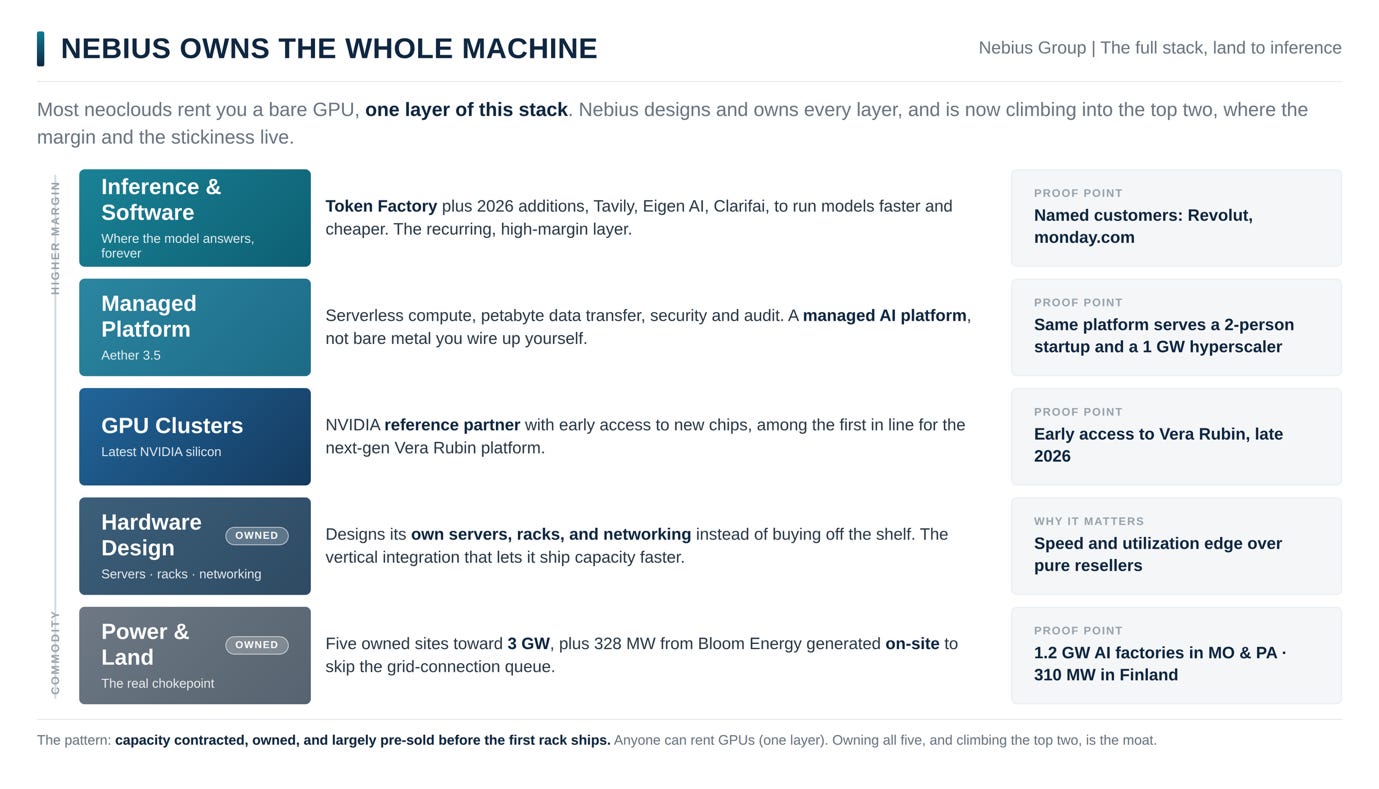

Full-stack, vertically integrated, and racing up the value chain

Most neoclouds just rent you a GPU. Nebius rents you the whole machine around it. It designs its own servers, racks, and networking, then layers its own software on top, so customers get a managed AI platform instead of bare hardware they have to wire up themselves. The flagship layer, Nebius AI Cloud, got more enterprise-ready with its March release, Aether 3.5: run a model without planning capacity in advance, move data across clouds at massive scale, and tighter security and audit controls. That range is the point. It can serve a two-person startup and a hyperscaler renting a gigawatt off the same platform, and management bets that software is what keeps customers sticky and margins high.

This is the difference between a landlord and a commodity wholesaler. Anyone with cash and a NVIDIA allocation can stack GPUs. The moat, if there is one, is speed, utilization, and software that makes the compute easy to use. It helps that Nebius is a NVIDIA reference partner with early access to the newest chips, including being among the first in line for the next-generation Vera Rubin platform in late 2026.

The more important shift is happening up the stack, in inference, the part where a trained model actually answers requests. Nebius spent 2026 climbing there through a mix of acquisitions and team-and-IP deals: Tavily (agentic search), Eigen AI (inference and model optimization, with technology NVIDIA ranked #1 at GTC 2026), and Clarifai, where it brought in the core team and licensed the inference IP for system-level orchestration rather than buying the company outright. Each added tools to run models faster and cheaper. The logic mirrors what Micron learned: training is the loud, headline-grabbing workload, but inference is the one that runs forever and pays a recurring, high-margin bill. Whoever drives down the cost per answer and makes deployment painless embeds themselves in the part of AI that never stops running. Nebius is bolting all of it onto Token Factory, its inference platform, which already counts Revolut and monday.com among its customers.

“The inference market is moving past raw GPU access. The real question now is who can turn open models into reliable, governed production systems with predictable cost, latency, and control.”

- Dylan Bristot, Product Marketing, Nebius Token Factory

The other half of the moat: power and land

You cannot conjure a gigawatt overnight, so Nebius plays two timelines at once: bring capacity online now, and lock land and power for years out. Its owned sites span the original Finnish data center, a New Jersey site serving Microsoft, two 1.2 GW “AI factories” in Missouri and Pennsylvania, and a 310 MW build in Finland set to be one of Europe’s largest. All told, five owned sites should deliver 3 GW. To power them without waiting in the grid-connection queue, now one of the industry’s worst bottlenecks, Nebius struck a deal with Bloom Energy for 328 MW generated on-site.

Power is the new oil here. Land with a live grid connection and a signed power contract is getting scarcer than the GPUs themselves, and whoever locked it early, before the rush and at the right price, owns the chokepoint. That is the whole Nebius pattern: capacity contracted, owned, and largely pre-sold before the first rack ships.

SECTION 5 · GROWTH CATALYSTS

What upcoming milestones could send this stock significantly higher?

Here is the thing about Nebius’s catalysts: they stack. That is what separates a hot quarter from a lasting re-rating, and it is why the timeline below reads as one chain rather than six scattered events.

The logic runs in order. Power comes online, fills up, and turns into run-rate revenue. That revenue compounds toward the multi-billion-dollar guide. A swelling contract book then converts the company from a volatile compute reseller, exposed to spot pricing, into something closer to a contracted utility, where every signed name lifts the revenue floor. And the part almost no one has put in a model yet is the move up the stack: as Nebius starts earning software and inference margin on top of pure rental margin, a capacity business quietly becomes a platform.

Each step de-risks the next. The capacity makes the revenue real, the contracts make it durable, and the software makes it more valuable. Miss one and the chain still mostly holds; hit all of them and a 684% quarter stops looking like a spike and starts looking like the first chapter. The timeline below is that chain, from the next earnings print to the destination it all points toward.

SECTION 6 · MACRO & INDUSTRY BACKDROP

The compute supercycle, and where Nebius sits inside it

The hyperscalers are spending hundreds of billions on AI through 2027, and chips are no longer the bottleneck. The real constraint is physical: building, powering, and cooling data centers fast enough to actually rack those chips. A GPU sitting in a warehouse, not plugged into a live, powered cluster, earns nothing. Neoclouds exist to close that gap, and demand is so fierce that even Microsoft and Meta are renting the overflow.

Geography cuts both ways for Nebius. Its Amsterdam base and European engineering core position it perfectly if Europe gets serious about building its own sovereign AI capacity instead of renting from American hyperscalers, an underpriced tailwind. The flip side is the Yandex heritage and the geopolitical baggage that trails it, which we will get to in the risks.

The sector’s bear case is simple and has played out before: compute pricing is not guaranteed. GPUs depreciate fast, everyone is building at once, and the moment supply catches demand, rental rates can roll over while the debt and depreciation keep grinding. Nebius’s answer mirrors Micron’s: contracted, supply-constrained, and largely spoken for today. Whether that holds as the whole industry builds is the entire question.

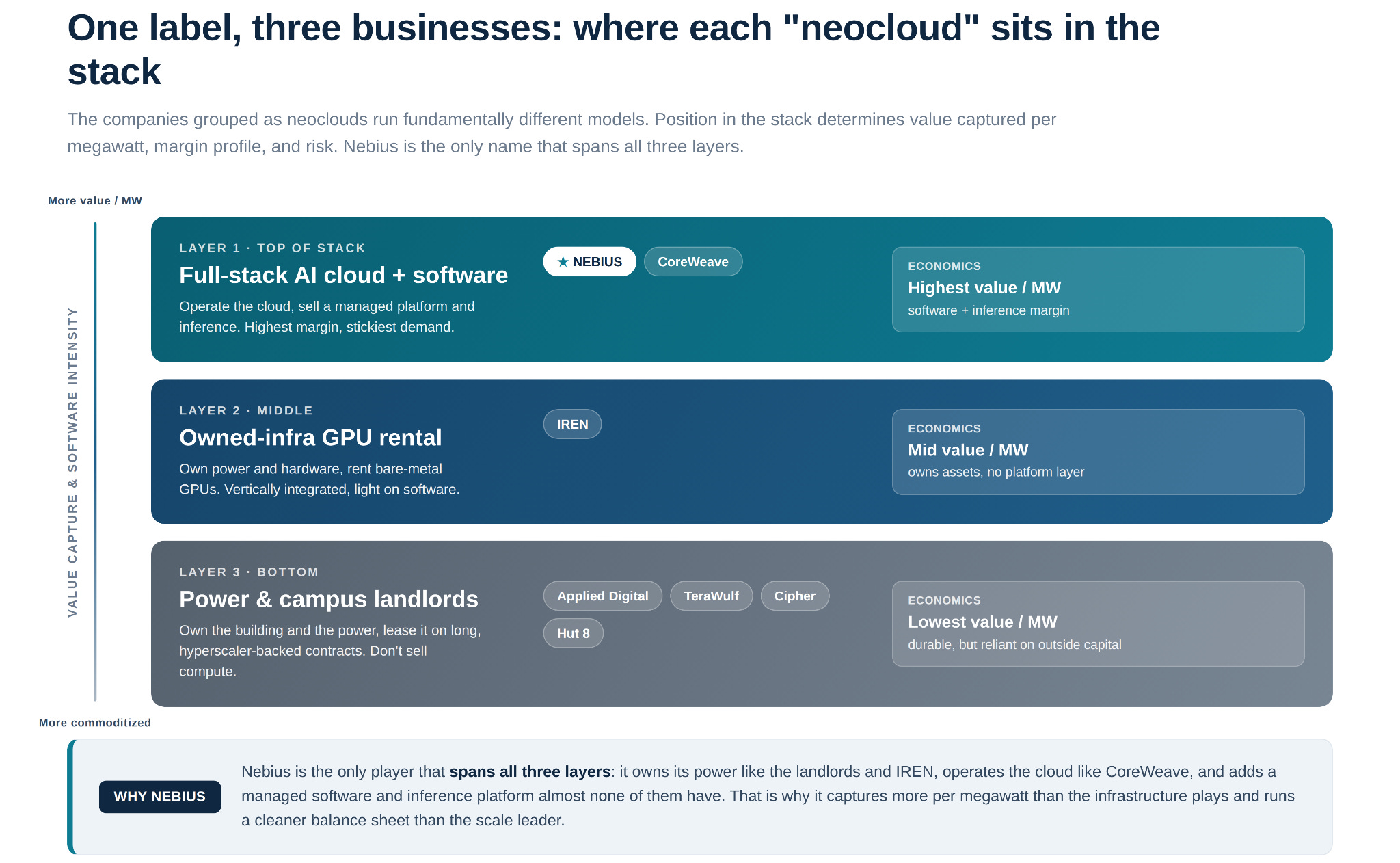

Where Nebius sits in the neocloud field

The trick to this sector is seeing that the companies lumped together as “neoclouds” run three different businesses. Picture a stack. At the top, you operate the AI cloud and sell software. In the middle, you own the hardware and rent out raw GPUs. At the bottom, you own the building and the power and lease it to someone else. Where you sit decides how much you earn per megawatt and how much risk you carry. Nebius lives at the top.

CoreWeave (CRWV) is the one to beat. It is the largest independent neocloud and the most entrenched with NVIDIA, with Q1 2026 revenue of $2.1 billion and a $99.4 billion backlog, and it earns the most per megawatt in the group. But the model is leveraged and asset-light: it leases its buildings from the likes of Equinix and Digital Realty and carries roughly $30 billion of GPU-backed debt, which is why its net loss widened to $740 million in Q1 even as revenue jumped 112%. Nebius is smaller but growing faster, owns over 75% of its own power, and runs a cleaner balance sheet, trading scale for ownership and durability.

IREN is the closest match, minus the software. Formerly bitcoin miner Iris Energy, IREN owns its power and sites like Nebius and has landed a $9.7 billion Microsoft contract plus an NVIDIA partnership targeting 5 gigawatts. The gap is the top of the stack: IREN rents bare-metal GPUs rather than selling managed software, and it shows in the economics. Nebius’s edge is the software layer IREN has not built.

The former miners (APLD, WULF, CIFR, HUT) are landlords, not rivals. They don’t operate an AI cloud or sell compute. They build campuses, deliver power, and lease it on long, hyperscaler-backed contracts: Hut 8’s 15-year, $7 billion Fluidstack lease backstopped by Google; Cipher’s nearly $5.5 billion AWS lease; TeraWulf’s Fluidstack deals with a $3.2 billion Google backstop; Applied Digital past 1 gigawatt contracted, much of it to CoreWeave. Sitting low means cleaner, longer-duration economics that dodge the GPU refresh cycle, but far less value per megawatt, lighter software, and heavy reliance on outside capital. These are Nebius’s suppliers and build-out peers, not competitors for the same customer.

So what sets Nebius apart? It is the only name that owns all three layers at once: power like the landlords and IREN, the cloud like CoreWeave, and a managed software and inference platform almost none of them have. That is why it earns more per megawatt than the pure-infrastructure plays and runs a cleaner balance sheet than the scale leader.

The honest caveat: none of this is a monopoly. Anyone with capital and a NVIDIA allocation can rack GPUs. Nebius’s moat is execution speed, owned power, utilization, and software, not physics the way it is for memory. Real edge, but only while it keeps out-executing a field racing just as hard.

SECTION 7 · RISKS

What could break this

Nebius just printed 684% revenue growth, a backlog near $46 billion, and a stock up more than 450% in a year. When a business is this hot, the risks do not vanish. They just get easier to ignore. So let us not.

1. The funding model is the business model. This one overrides the rest. Nebius is guiding to $20-25 billion of capex against barely $3 billion of revenue, raised over $6 billion in Q1 alone, and doubled its debt to $8.4 billion in a single quarter, with more borrowing already flagged. The entire machine depends on raising capital, over and over, on terms that do not gut the equity. If AI funding tightens or the cost of capital spikes, the buildout stalls and the contracts get harder to honor. The bull case quietly assumes the money always shows up. History says be careful with that.

2. Two customers are most of the backlog. Microsoft and Meta dominate that $46 billion book. Wonderful while they are hungry, dangerous the moment one slows, renegotiates, or decides its own data centers have caught up, and both are building in parallel. There is not much cushion underneath. Note too that up to $15 billion of the Meta deal is capacity Nebius can reallocate, flexible, but not a hard, dedicated purchase.

3. The financing loop looks circular. NVIDIA puts $2 billion into Nebius, then Nebius buys NVIDIA GPUs. It is the same loop running through most of the AI buildout, and it makes demand look more independent than it is. Nothing improper, but part of the “demand” is the supply chain funding itself, and that can unwind fast.

4. Compute is closer to a commodity than memory. Only three companies on Earth can make HBM. Far more can rack GPUs. Nebius’s edge is speed, utilization, and software, not physics. CoreWeave and the hyperscalers are in the same race, so if rental rates compress, there is no structural monopoly protecting margins.

5. Depreciation, and a small accounting tell. GPUs lose value fast, on roughly a four-year clock. Starting Q1 2026, Nebius stretched the assumed life of its servers from four years to five. That lowers depreciation each quarter and flatters margins, defensible if the gear really lasts, but exactly the kind of estimate a skeptic watches. And if AI demand pauses, Nebius is left with billions in hardware depreciating against contracts that may not all get honored. The asset base does not forgive an air pocket.

6. Valuation prices perfection. At roughly 65 times sales, the stock cannot survive a single soft quarter unscathed. It ran from a 52-week low near $44 to $300, and a stock that climbs like that can give a lot back fast on any wobble.

7. Heritage, governance, and execution. The Yandex origin carries geopolitical baggage outside management’s control, governance scores poorly, and Volozh keeps outsized voting control through special shares. On top of that, scaling live power roughly six-fold in a year while digesting several acquisitions is a lot going right at once. Any one slip is survivable. Several together compress the story.

Bear case in one sentence: you are paying 65 times sales for a capital-hungry compute provider whose backlog leans on two customers, whose margins depend on a commodity staying scarce while everyone builds, and whose growth plan needs billions more raised on friendly terms.

The counterweight is not small: demand for compute is outrunning supply so badly that the companies who build data centers for a living are renting from Nebius instead. If that holds, a stumble just slows the growth rate. If it cracks, it is a long way down from 65 times sales.

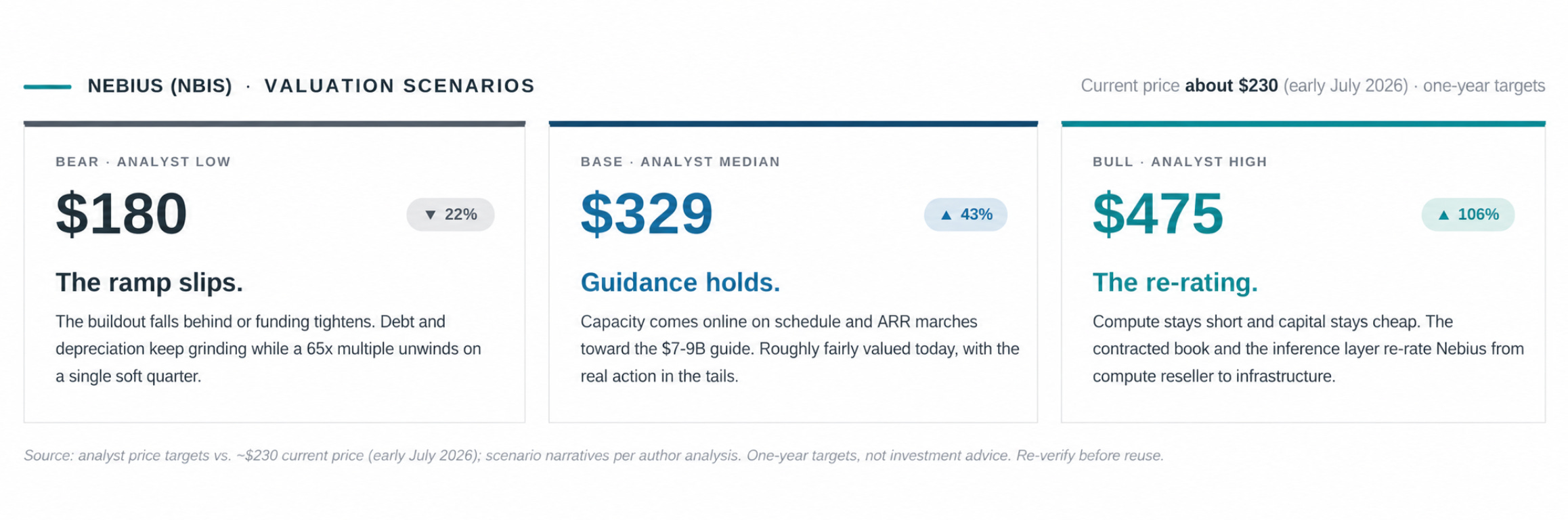

SECTION 8 · VALUATION & PRICE TARGETS

Cheap is not the word. The question is whether the ramp earns the multiple.

Near term, value it on ARR. At about $230 (early July 2026), Nebius is worth roughly $60 billion, about 31 times its current $1.92 billion run-rate. Expensive on its face. But here is the bull’s move: management guides that run-rate to roughly quadruple, to $7-9 billion exiting 2026. Hit that, and the same $60 billion price tag is only about 8 to 10 times run-rate for a company still compounding fast. Suddenly it is not expensive at all. It is cheap for the growth. The argument in one line: do not value Nebius on the run-rate it has, value it on the one it is about to reach.

The bear’s answer is just as simple. A guide is a promise, not money in the bank. That $7-9 billion rides on capacity not built yet, funded by capital not raised yet, sold to two customers building their own in parallel. Pay 31 times today’s run-rate and you are not buying the ramp, you are underwriting it. The market has watched compute get overbuilt before. This multiple is not the market calling Nebius cheap. It is the market betting the buildout lands.

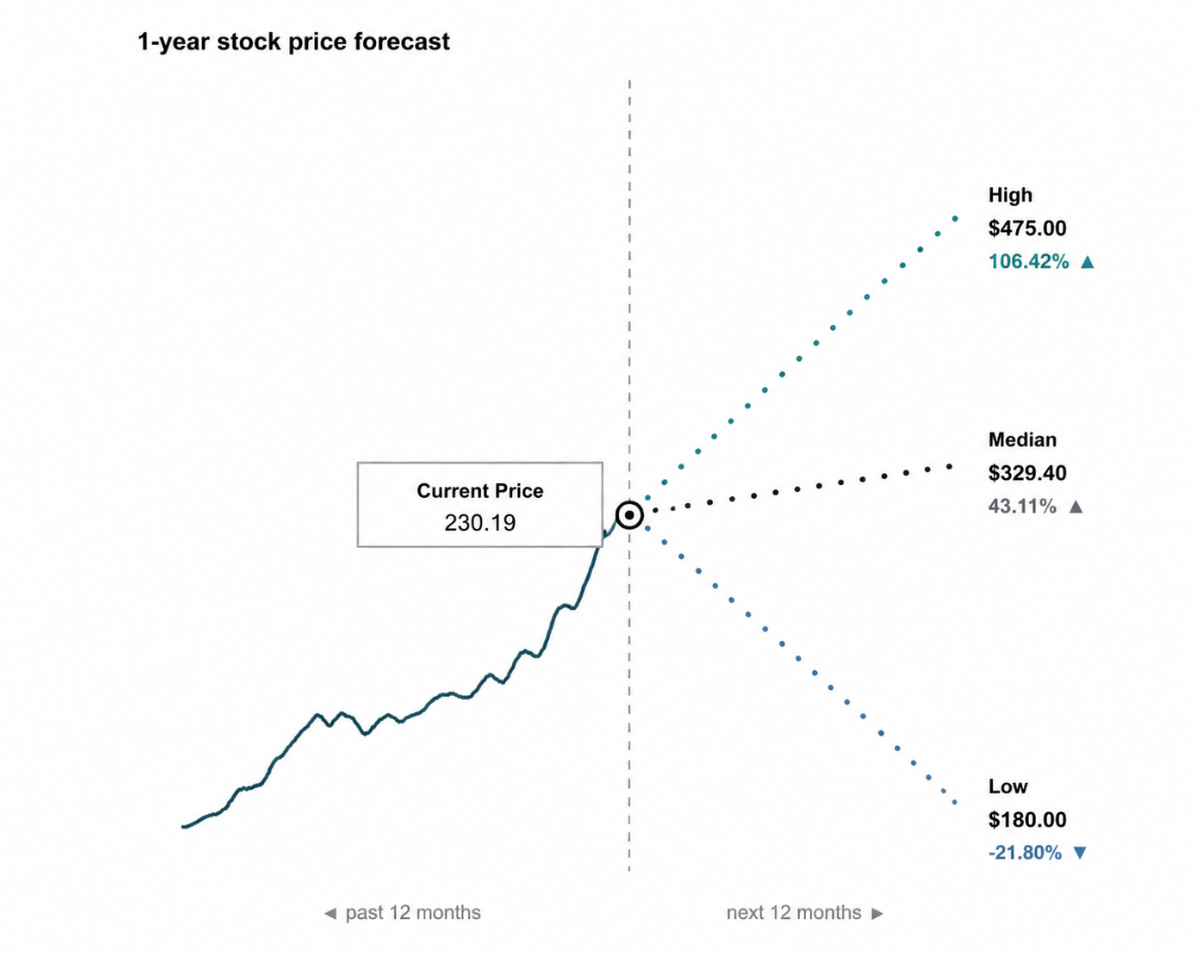

You can see that bet in how far apart the price targets sit: a low of $180, a high of $475, a median of $329.40. That is not a forecast, it is the argument priced two ways. The high is the ramp landing clean; the low is it slipping while debt and depreciation grind on. The median sits about 43% above today’s price, a real but modest base case, with all the real action still in the tails. A year ago the average target was near $55. The easy mispricing is gone. From here, Nebius has to earn it on delivery.

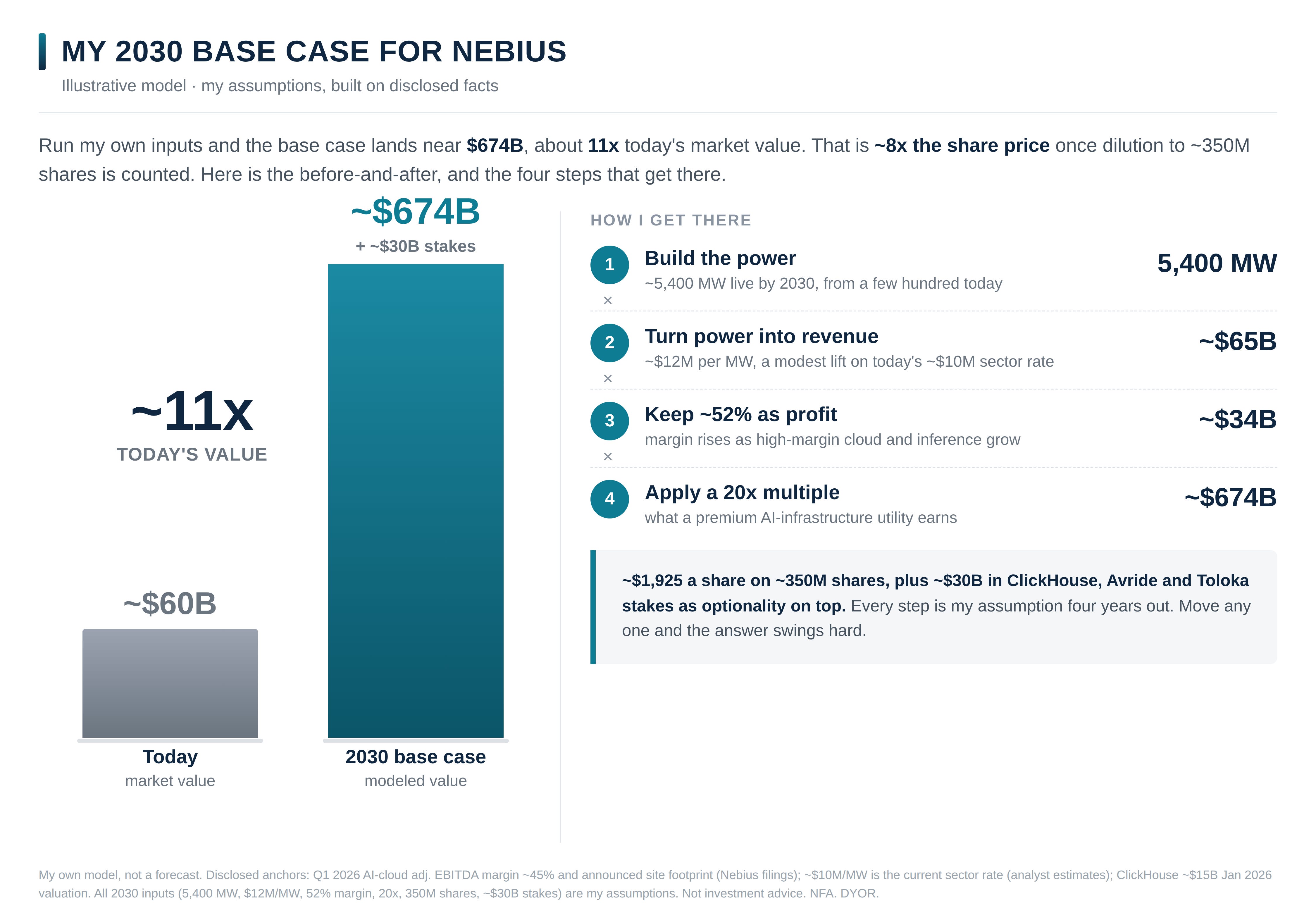

Long term, the yardstick changes. Sales multiples are a near-term lens. As Nebius matures and its depreciation bill balloons, all those GPUs and buildings wearing down on schedule, the better measure becomes EV/adjusted EBITDA, the standard for capital-heavy infrastructure. So the 2030 case has to be built on profit, not revenue, with one caveat stamped on every line: these are assumptions four years out, and even the base case bakes in near-flawless execution.

Three inputs drive it. Capacity: roughly 5,400 MW of active, revenue-generating power by 2030, up from a few hundred today, which already assumes no serious delays at the big US sites (Pennsylvania, Independence, Vineland), the single biggest risk to the number. Revenue per megawatt: about $12 million, a modest lift on today’s rough $10 million sector standard. That math is roughly $65 billion of 2030 revenue. Margin and mix: the subtle one. The Meta and Microsoft deals are lower-margin bare-metal work, fixed pricing with the customer doing everything except plugging in the GPUs. The case needs Nebius to keep tilting revenue toward its own higher-margin cloud (today the split is around 50/50). Do that, and the margin rises as high-margin cloud and inference grow, landing near 52%, which on $65 billion is about $34 billion of adjusted EBITDA.

Put a 20x multiple on that, the “AI infrastructure becomes a utility” case, rich but defensible for a grower this central, and you land near a $674 billion enterprise value. Since debt and cash should roughly cancel by 2030, that is also the market cap, before counting strategic stakes like ClickHouse (Nebius owns about 25%), Avride (about 83%), and Toloka, which the model pencils at another ~$30 billion.

Against today’s ~$60 billion, that base case is about eleven times the current company, and even after dilution the implied 2030 share price is roughly eight times today’s price, near $1,925 a share on ~350M shares. That is the number that makes people lose their minds, so here is the discipline: it still assumes the buildout lands, the mix shifts, the funding stays cheap, and the AI cycle compounds for four more years. Move any one input and the output swings hard.

So is it cheap? Not on anything you can hold today. It is cheap only if you trust the ramp, the buildout behind it, the funding behind that, and the customers anchoring it all. The question was never whether the business is growing. It is whether that growth is fundable and durable enough to grow into a price this rich, this year and for the four after it.

SECTION 9 · TRADING THE NEWS

Meta wants to be a cloud provider, too

The two-way read. Bloomberg reports Meta is building a cloud business to sell access to its AI computing power and models, aimed straight at AWS, Azure, and Google Cloud. It cuts both ways for Nebius, and both are true. Bullish: even Meta, sitting on one of the largest GPU fleets on earth, now sees selling compute as a business worth entering. That is the whole Nebius thesis, compute is the product, said out loud by a hyperscaler. Bearish, and sharper: Meta is Nebius’s largest single contract at roughly $27 billion, and a customer that starts reselling compute is a customer drifting toward competitor. It hardens a risk already on the board, your two biggest names are building in parallel.

Bottom line. Near term, nothing breaks. Meta signed Nebius because its own buildout is behind, and standing up a commercial cloud business takes years, so the $12 billion of dedicated capacity is still needed on day one. This is the risk turning concrete, not detonating. It also makes the flexible leg of the deal, the up to $15 billion Nebius can resell, look smart in a world where Meta wants optionality on its own compute. The line to watch: whether building in parallel quietly becomes buying less from Nebius.

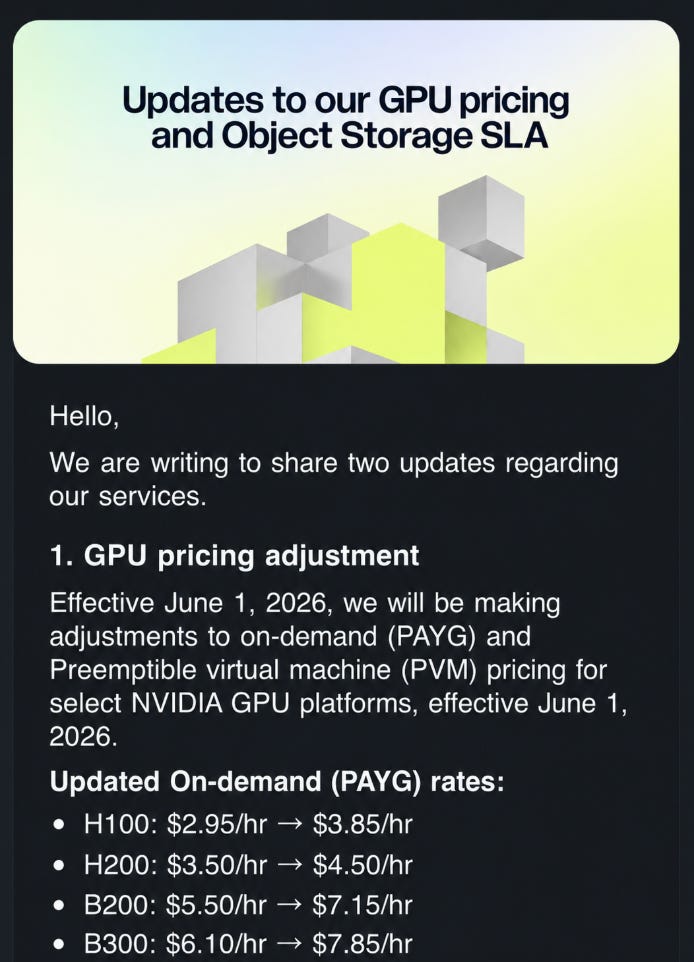

The price hike nobody had to model

Most of this thesis runs on guidance and backlog, numbers management chooses to show you. This one is different. In May, Nebius customers received an email informing them that on-demand GPU prices were going up, and it laid the demand story bare: effective June 1, standard on-demand pricing rose roughly 30% across the board. H100 went from $2.95 to $3.85 an hour, B200 from $5.50 to $7.15, with similar jumps on H200 and B300. The spare-capacity tier (preemptible, the cheaper option you take when you can tolerate interruptions) rose even more, some rates up 70%.

Why it matters. In a commodity market, you do not raise prices 30%. You cut them to win volume. Nebius did the opposite: it raised them, told customers it still offers some of the most competitive pricing around, and nudged them toward locking in reserved capacity instead. That is not a company fighting for demand. It is a company with more demand than supply, rationing it by price. And in this model the increase is almost pure profit, because the data center is already built, the GPUs already racked, the power already paid for. Charge 30% more for the same hour of compute and most of that extra dollar falls straight to the bottom line. It is the cleanest confirmation yet of the “supply problem, not a demand problem” line management repeats every quarter, except this time it came straight to customers, not from a podium.

The bear note. It is one snapshot, on a handful of chips, and it does not translate cleanly to the blended price across the whole book. The Microsoft and Meta deals, most of the contracted revenue, are locked at fixed terms and do not move when the on-demand sheet does. A list-price bump on spot capacity is real, but it is the smaller, more volatile slice of the business. Read it as a signal, not a margin model.

My take. Guidance can be sandbagged and backlog can be front-loaded, but a price increase sent to paying customers is the one number management cannot dress up. It is the market clearing in real time, and it cleared higher. Until the on-demand sheet starts moving the other way, the crunch is real and the pricing power is Nebius’s. The customers are paying up. That is the tell.

SECTION 10 · THESIS SUMMARY & VERDICT

My verdict on $NBIS: own it, but size it like the high-beta name it is.

Strip away every chart and quarter and the whole story is one sentence: the companies that build data centers for a living have decided it is faster to rent from Nebius than to wait on themselves. That is the tell that matters. You do not outsource your own core competency to a startup unless the shortage is brutal and the startup is genuinely better at the one hard thing. Nebius is better at it because it sits at the top of the neocloud stack, owning its power, running the cloud, and building into software and inference, where almost nobody else holds all three. You cannot fake a powered gigawatt, and you cannot bolt on a software layer in a quarter. That is the moat.

Now the part the run obscures. This is not a business that wins by being right once. It wins by raising money, building, filling, and then raising again, dozens of times, without ever paying too much for the capital. Capex is guided to $20-25 billion against barely $3 billion of revenue. The contracts are gorgeous, but two customers carry most of the book, and both are building their own capacity beside it. So the thing you are actually buying at roughly $230 is not the business as it exists. It is your confidence in the next twelve raises and the next two years of execution. Get that wrong and the most beautiful backlog in the sector becomes a liability schedule.

That is why I think about this position as a dial, not a switch. The stock has already traveled $44 to $300 and back to $230 in a year, and it will keep moving like that, because every print either confirms or threatens the ramp with nothing in between. So I hold a core and I feed it on the ugly red days, when the funding fear is loudest and the price is cheapest, never on the green ones. A name like this can shed 30 to 40% on a single soft quarter, and the whole point is to still be holding when it does.

One myth to kill, because it sets you up to be disappointed. People want this to be the “next Nvidia,” a company protected by a product only a handful of firms on Earth can physically make. It is not. Anyone with capital and a NVIDIA allocation can stack GPUs. Nebius has no chemistry monopoly, and its edge is execution, not physics: it ships faster, owns its power, and holds the cleanest contracted book among the independents. That edge is real but fragile, because it lasts only as long as it keeps out-running a field sprinting just as hard. Do not buy this expecting a moat made of physics. Buy it expecting a moat made of speed and software.

So where does that leave the price? The market is paying up for the contracts it can already see and almost nothing for the part I believe in most: Nebius is becoming the AWS of inference, and inference is forever. Training is the loud one-time headline. Inference is the workload that never switches off, every query and every agent, billed by the second for as long as the model runs. And here I stop being an analyst and become a customer. The shortlist for serious AI compute used to be Microsoft, Google, and AWS, full stop. Not anymore. Nebius has entered that conversation, and I am seeing it happen from the buyer’s side of the table, not off a pitch deck. That leg is in almost nobody’s model. Neither are ClickHouse, Avride, or Toloka. If the buildout lands and money stays cheap, today’s price is a fraction of what this becomes. If either breaks, it unwinds fast, and debt and depreciation do not wait for the story to heal. Both paths are live. That is the trade.

I am long, with conviction and a leash. Sized to survive a bad print, never chased on a good day, never left alone.

Long NBIS. High conviction, high beta, sized accordingly.

DISCLAIMER

This analysis is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any security.

July 1st, 2026 | Price: ~$230 | Sources: 20-F · 6-K · Q1 FY2026 Earnings Call · Q1 FY2026 Shareholder Letter | NFA. DYOR.

“It ran from a 52-week low near $44 to $300, and a stock that climbs like that can give a lot back fast on any wobble.”

Exactly one of the reasons why stocks like this should be DCA in instead of bought entirely. Was down 15% on yesterday’s Meta news.

Also the discrepancy in price targets was huge, important to include… I do think the bear case should be well under $100. (Bear case if everything goes wrong).

Seems like a solid company to add as a high upside risky pick (3-5%). Anything more seems a little risky for me, anything less probably isn’t worth it.

Overall, fantastic article and really appreciate you putting the time and effort into writing this.

I see it touching 190 from my own analysis. And if that fails too, I think you might have to wait few weeks before people posting about NBIS goes ballistic. Let's see if it even holds current 229. You should put your seat belts on Ren!!!.