$MU - Micron: It didn't pivot to AI. AI came looking for it.

A 47-year-old DRAM maker that spent decades getting crushed by the memory cycle. Then the GPUs ran out of memory.

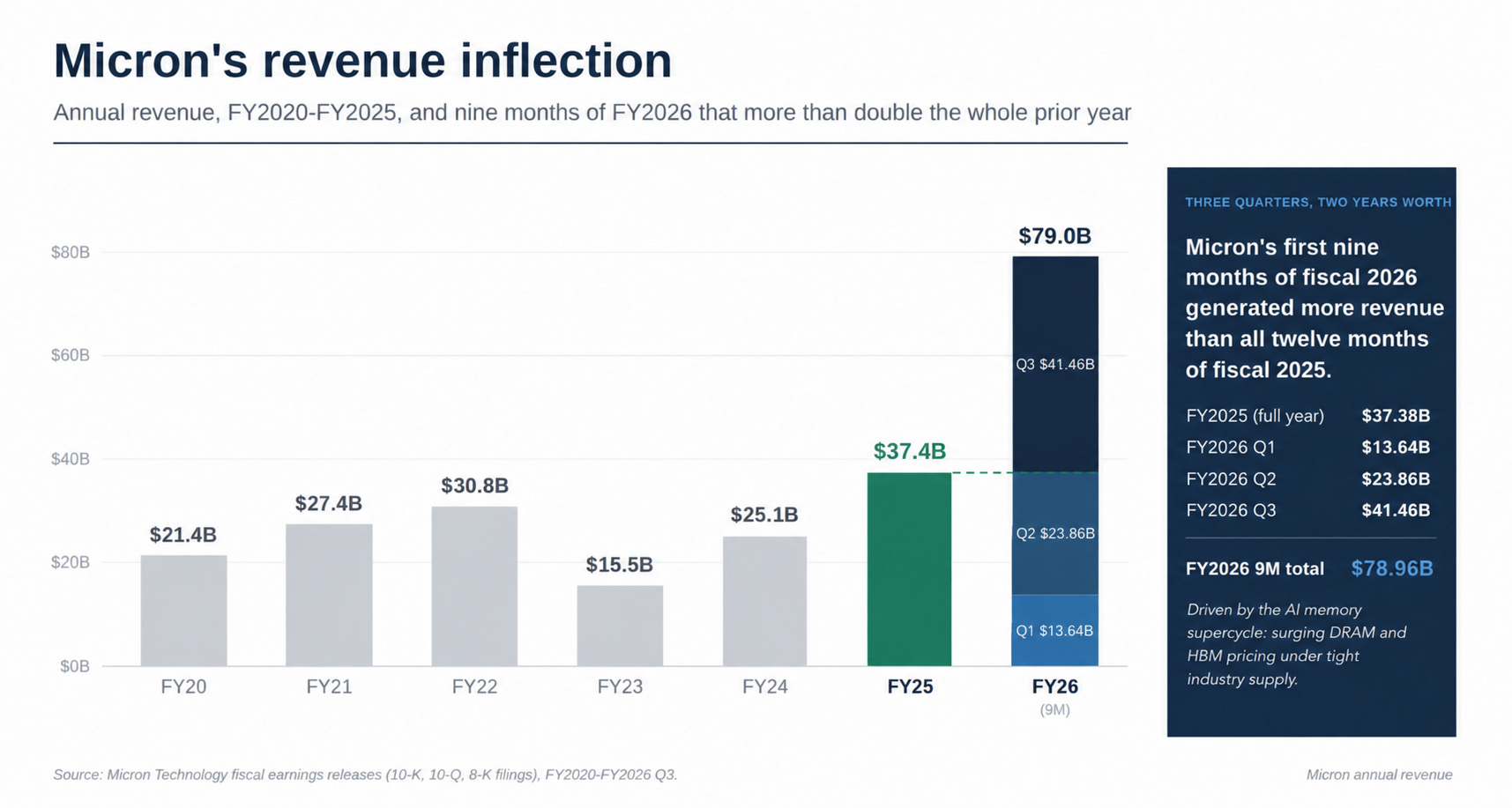

From $69 a year ago to ~$1,048 heading into this print, up over 1,000% in twelve months, crossing $1 trillion in market cap along the way. The print just landed, and it didn’t clear the bar. It detonated it. Micron guided to $33.5 billion. It delivered $41.5 billion. EPS was guided to ~$19. It printed $25.11.

BEFORE WE DIVE IN

Micron sits at Layer 6: Memory. The model weights, the training data, the context window your prompt just filled up, the cache that lets a chatbot answer you in milliseconds: none of it lives inside the GPU itself. It lives next to it, on chips built for one job, holding data and moving it fast enough that the GPU never has to sit around waiting.

Micron doesn’t just sell a component in the AI stack. It controls one of the scarcest inputs in the entire buildout, the memory every accelerator, every hyperscaler, and every frontier AI lab on Earth cannot get enough of.

There is no AI training run without DRAM feeding the GPU in real time. There is no AI accelerator at scale without HBM stacked directly on the package. Micron makes both.

Sanjay Mehrotra, Chairman, President and CEO, put it plainly on September 23, 2025: “As the only U.S.-based memory manufacturer, Micron is uniquely positioned to capitalize on the AI opportunity ahead.”

Before we go further, a quick note on the alphabet soup. Headlines throw around DRAM, NAND, and HBM like they’re interchangeable. They’re not, and the difference is the whole reason Micron’s stock looks the way it does right now.

The fastest GPU in the world is useless if it’s sitting idle waiting for data, and that’s exactly the problem with training and running today’s massive AI models: moving information back and forth eats up more time than the actual computing. HBM fixes this by stacking memory chips directly on top of the GPU, like moving your desk into the room where all the files are kept instead of down the hall. That proximity is why it’s become the real bottleneck in the AI race: you can have all the computing power in the world, but without enough HBM, it just sits there waiting. And unlike regular memory chips, HBM can’t be swapped in from any supplier on short notice. It takes months of testing to qualify a new one for a specific chip design. That’s why the companies that make it have buyers locked into contracts years out. HBM didn’t just get faster, it became the thing standing between “we have an idea for an AI model” and “we can actually build it.”

SECTION 1 · COMPANY SNAPSHOT

What is MU and why did it just cross $1 trillion?

Founded in 1978 in Boise, Idaho, by brothers Ward and Joe Parkinson and two colleagues, it spent the next 47 years as one of the most cyclical names in tech: prices spike, the industry overbuilds, prices crash, and the stock round-trips with it, profitable one year, bleeding cash the next. Wall Street priced it like a commodity, because for most of its history, that’s what it was.

AI broke that pattern. Once memory became the bottleneck standing between every AI lab and the chips it needed, Micron’s customers stopped haggling on the spot market and started locking in multi-year supply contracts instead. Micron’s entire 2026 production sold out before the year even started.

Headquartered in Boise, Idaho, with fabrication and assembly operations across the US, Taiwan, Japan, Singapore, Malaysia, China, and India, Micron trades as $MU on Nasdaq. Fiscal 2025 revenue hit a then-record $37.4 billion, up 49% year over year. Fiscal Q2 2026 came in at $23.86 billion, up 196% year over year. Then fiscal Q3 2026 didn’t just hit the $33.5 billion guide. It blew through it. Revenue landed at $41.5 billion, up 74% sequentially and 346% year over year. One quarter of revenue now exceeds Micron’s entire annual revenue in any fiscal year through 2024.

Wall Street noticed long ago. The stock ripped over 1,000% in a year, and in 2026, Micron crossed a $1 trillion market cap, becoming a trillion-dollar company almost nobody would have predicted for a memory chipmaker a few years earlier.

The 47-year-old commodity company is now one of the most fought-over names in the AI supply chain.

SECTION 2 · FUNDAMENTALS

How does it make money and who’s running the show?

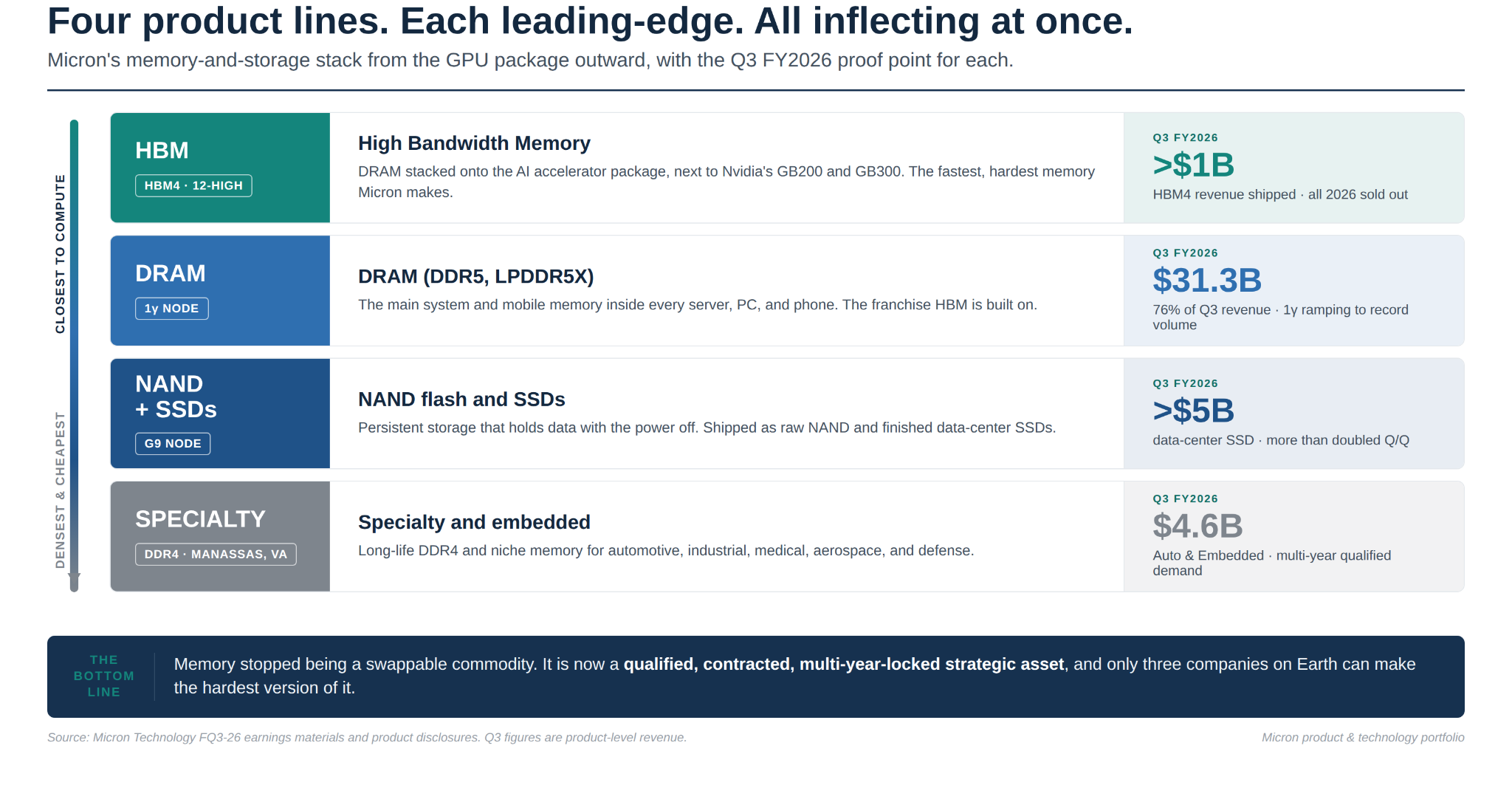

Micron organizes its business into four units: Cloud Memory (hyperscale cloud and all data-center HBM), Core Data Center (mid-tier cloud, enterprise, OEM, and storage), Mobile and Client, and Automotive and Embedded. Right now, the data center is the entire story. Data center revenue exceeded $25 billion in fiscal Q3 alone, an annualized run rate of over $100 billion. Data center SSD revenue exceeded $5 billion, more than doubling sequentially.